![The orbiting solar module captures the Sun’s delicate corona in stunning detail [Video]](https://scitechdaily.com/images/ESA-Solar-Orbiter-scaled.jpg)

Justin Sullivan

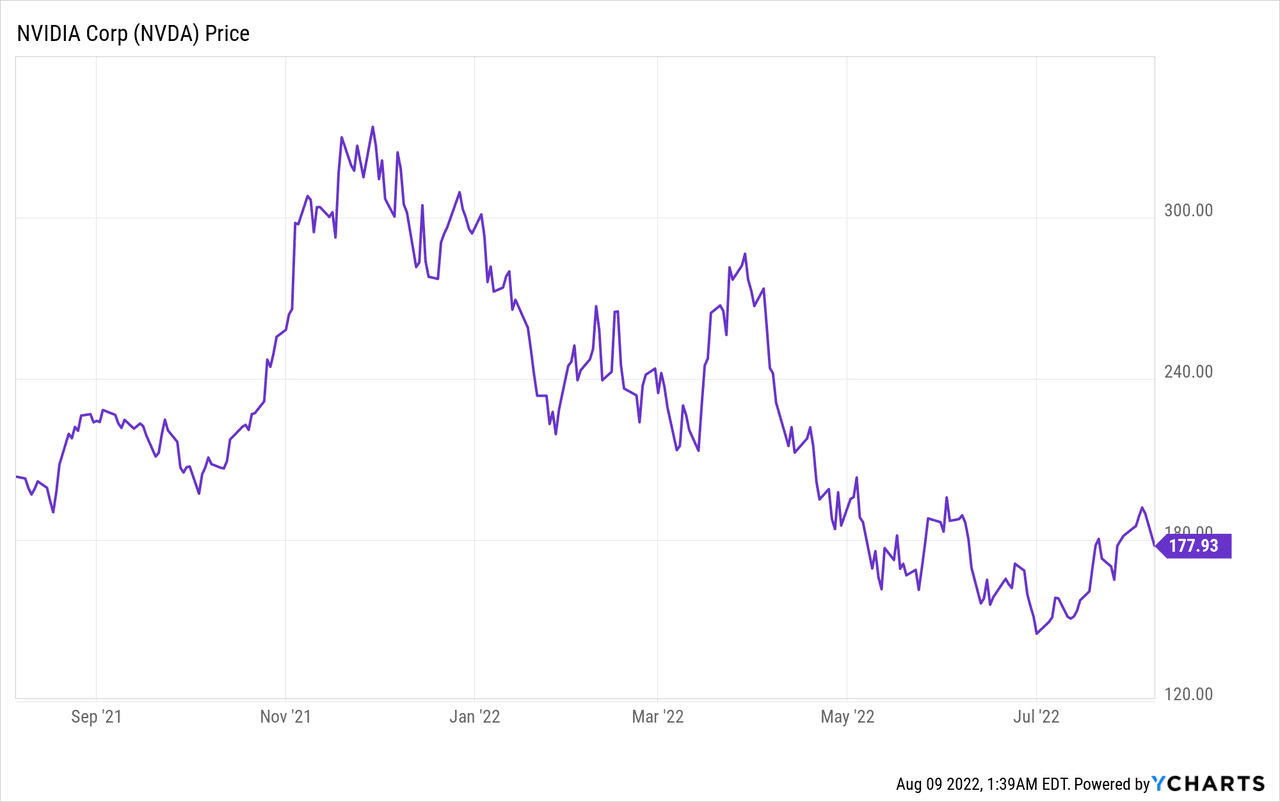

nvidia (Nasdaq:NVDA) is a leading manufacturer of graphics cards for gaming, data center computing, visualization, and automotive semiconductors. It’s known as a true “growth stock” after revenue has previously grown at a compound annual growth rate of nearly 50% over the past five years (up to Q4421). However, the company It recently announced its preliminary financial results for the second quarter ending July 31, 2022. Revenue came in below analyst estimates, due to a lack of gaming revenue. I previously wrote a post on Microsoft (MSFT) and its second-quarter earnings that also showed lower demand for games, so this post could have been a leading indicator of Nvidia’s poor results. Nvidia’s stock price is down nearly 6% in the news and has slaughtered 46% from all-time highs in November 2021. The good news is that the company still has best-in-class technology and a strong chance of recovery due to the cyclical nature of the gaming market. In this post, I will detail the latest earnings report and Nvidia valuation calculation. Let’s dive in.

Nvidia Q2 detail

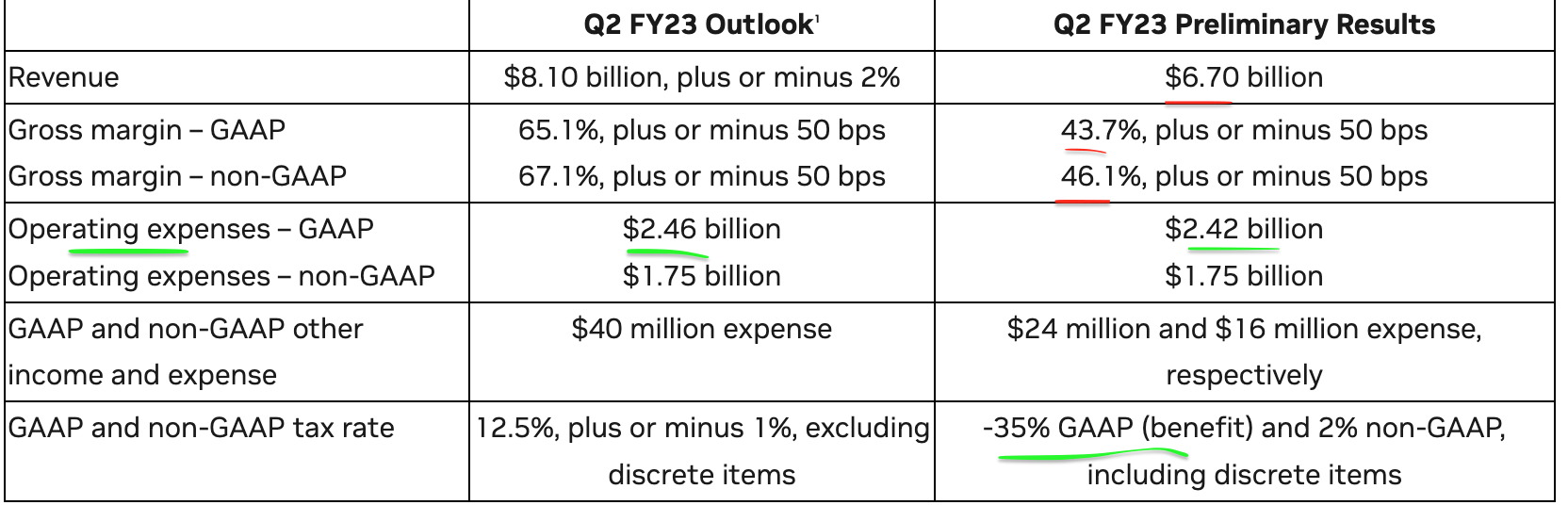

nvidia mentioned $6.7 billion in revenue for the second quarter of 2022, which was well below the previous forecast of $8.1 billion. Revenue is also down a whopping 19% since last quarter and up just 3% year over year. This decline in revenue was primarily driven by a sharp drop in gaming revenue, which amounted to $2.04 billion, down 44% sequentially and 33% yoy.

Intel Corporation (INTC) has the largest part of the graphics processing unit (GPU) market, with a market share of 60%. However, Nvidia and AMD (AMD) gradually eating up Intel’s GPU market share. Nvidia is the leader in “high performance” GPUs and has a market share of 21% of the total market, up from just 15% in Q1 21. This is evidence of Nvidia’s best-in-class technologies.

GPU Market Share (John Pedy Research)

It’s easy to fall into one bad quarter of Nvidia’s low gaming revenue, but I think it makes sense to scale back. The gaming market is cyclical and is expected to grow at a compound annual growth rate (CAGR) of 31.87% fast through 2028, when it is expected to reach a value of $165 billion. Thus, despite the macroeconomic headwinds in the short term, I think Nvidia is in a strong position to recover in the long term. Additionally, a portion of Nvidia’s GPU revenue came from purchases of Bitcoin mining rigs in 2020/2021. However, now that the price of the cryptocurrency has fallen and we are now in the “Bitcoin Winter”, sales in this area will of course decrease. Nvidia has been criticized in the past for not reporting its GPU revenue which came directly from Bitcoin mining hardware sales. The company was recently fined by the Securities and Exchange Commission for not doing so Reports GPU Sales Driven by Bitcoin in First Crypto Bubble/Crash of 2017.

“NVIDIA’s disclosure failures have left investors with information critical to evaluating the company’s business in the key market” — Christina Littmann, SEC Crypto Unit.

So, assuming higher-than-normal GPU sales in 2020 and 2021, from both the boom in gaming and coding, the patch now wouldn’t be surprising.

Nvidia’s management stated that gaming revenue was lower than expected, reflecting “lower channel partner sales due to macroeconomic headwinds.” However, they have implemented inventory adjustments and “pricing programs” with channel partners to reflect market conditions. I think these “pricing programs” are a series of discounts that will of course affect Nvidia’s financials.

Nvidia segment revenue (Financial results for the second quarter)

Nvidia’s data center revenue was $3.81 billion in the second quarter. The growth rate slowed to just 1 percent from the previous quarter, but was still up 61 percent year over year. The company stated that the recent slowdown was due to “supply chain disruptions,” but I also suspect that macroeconomic conditions have caused temporary cuts in IT spending by companies.

The good news is the data center industry Expected To grow at an astounding $615 billion between 2021 and 2026, or a compound annual growth rate of 21.98%. This growth is expected to be primarily driven by the North American market as companies “digitalize” to the cloud. So, despite the recent headwinds, Nvidia has a broad growth path for its data center segment. Nvidia is also specialized in AI-based computing, which is another fast thing grow industry.

Professional Visualization revenue was $500 million, down 20 percent sequentially or 4 percent year-over-year. However, auto revenue showed strong momentum at 59 percent sequentially and 45 percent year-over-year.

Revenue vs. expectations (NVIDIA earnings)

Nvidia’s ultra-high gross margin of 65% was compressed to 43.7% in the second quarter, but management believes its “long-term gross margin profile is sound.” Nvidia also controlled its operating expenses very well, coming in below its $2.46 billion forecast, with $2.42 billion.

Nvidia CFO (Colette Chris)

“We plan to continue with our share buybacks as we anticipate strong cash generation and future growth.”

Management is expected to discuss full financial results and expectations for a previously planned August 24 earnings call.

Advanced evaluation

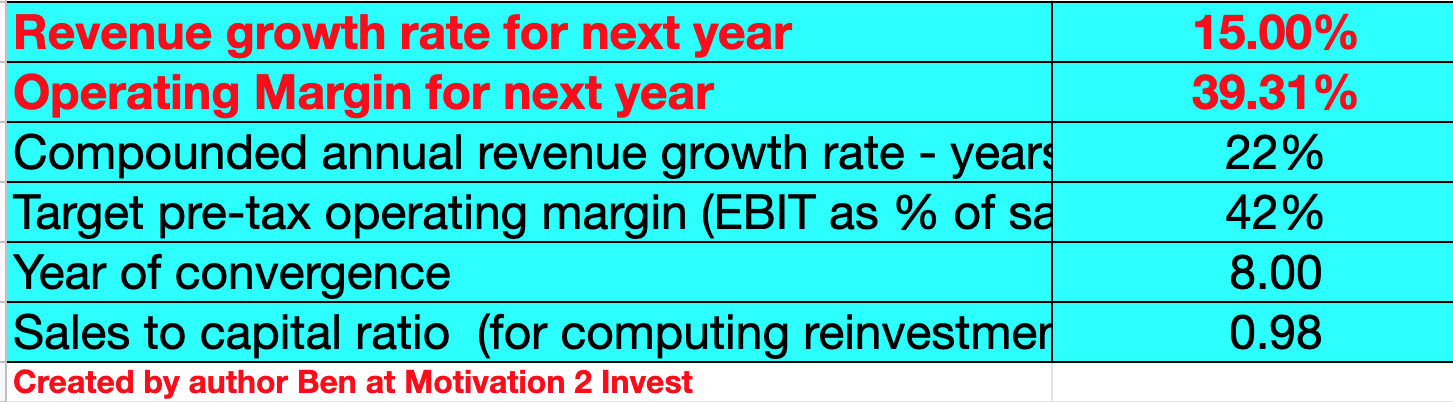

In order to valuate Nvidia, I plugged the most recent financial data into my advanced valuation form, which uses the discounted cash flow method for valuation. I’ve lowered my revenue growth forecast from previous rates of 30% to 40% to a conservative 15% growth rate for next year. Revenue growth then doubled by 22% over the next two to five years. This is assuming a cyclical recovery in gaming revenue, data center revenue continuing to grow according to the trend year over year and auto revenue growing strongly.

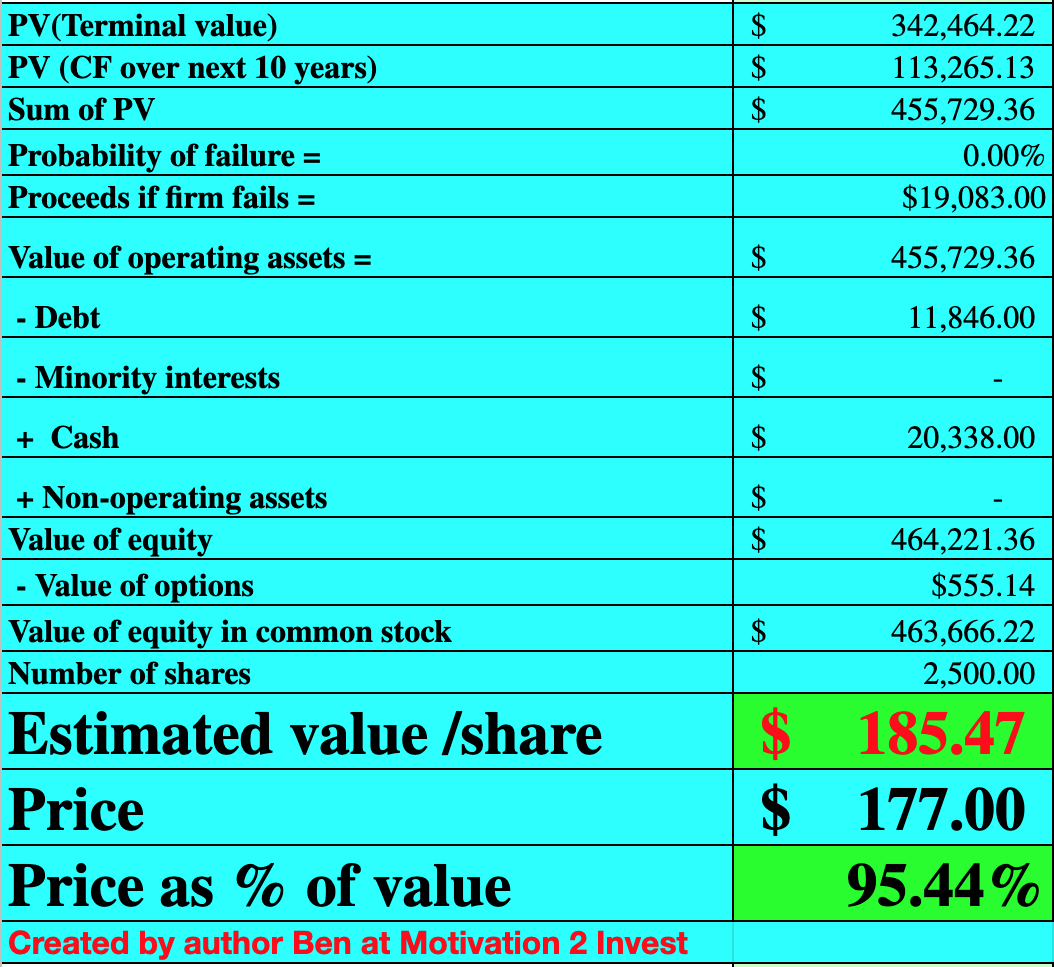

Nvidia Stock Rating 1 (Created by author Ben at Motivation 2 Invest)

I’ve also forecast that Nvidia’s operating margin will rise to a healthy 42% over the next eight years as data center and visualization revenue grows robustly. In order to increase the accuracy of the assessment, I capitalized the company’s research and development expenditures.

Nvidia stock valuation (Created by author Ben at Motivation 2 Invest)

Given these factors, I get a fair value of $185/share. The stock is currently trading at $177 and is therefore roughly 5% undervalued with these long-term growth estimates.

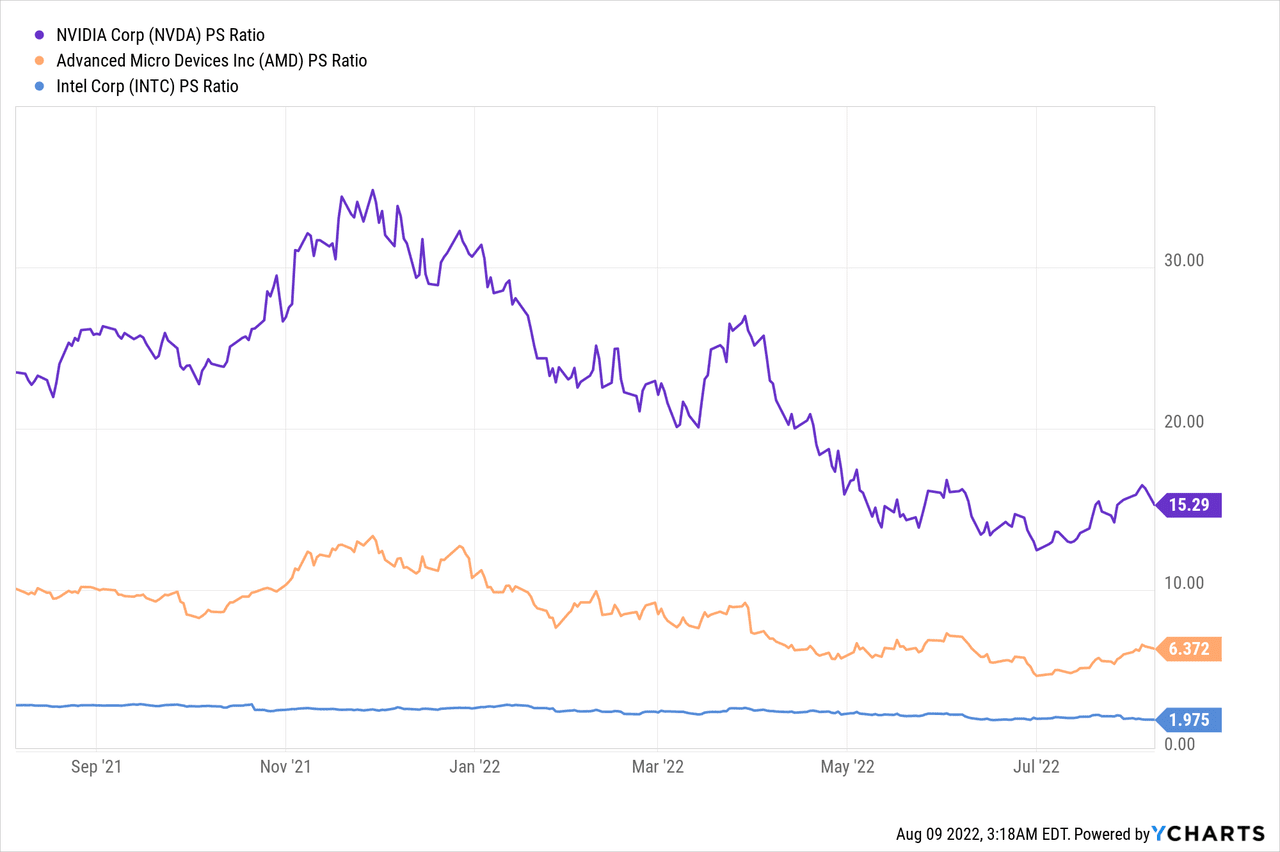

As an additional data point, Nvidia is trading at a price-to-sales ratio (FWD) = 14.23, which is about 2.75% lower than the five-year average. Therefore, the stock is “fair value” based on the price-to-price ratio. Nvidia trades with a higher price-to-sales ratio than AMD and Intel, but also has much higher profit margins.

Risks

Low Spending / Recession on IT

High inflation and high interest rates environment It increases input costs for businesses, so we may see a temporary reduction in IT spending for at least the next two quarters. ‘Stagnation’ is also Expected Which will affect consumer sentiment and reduce spending. Low crypto prices are also a negative for Nvidia, as it means that fewer GPUs will be purchased for Bitcoin mining platforms.

last thoughts

Nvidia is a technology leader and the second largest provider of gaming GPUs. The company’s high-performance technology is best-in-class, but I think this quarter (and possibly the next) will be down due to macroeconomic headwinds. However, it does make sense to remember that the long-term growth trends in datacenter, gaming, and even “Metaverse” visualization are not going anywhere. Nvidia is fairly valued at current levels, but I expect a lot of volatility in the next quarter for the recovery to show itself.

“Typical beer advocate. Future teen idol. Unapologetic tv practitioner. Music trailblazer.”

More Stories

Shiba Inu vs Avalanche: Does AVAX threaten SHIB’s base?

James Cameron and Ari Emanuel lend support to the Skydance-Paramount show

Yellen advises caution about currency intervention after the yen rises